“Banks’ progress in managing climate- and nature-related risks”

(Source: European Central Bank, Good Practices for Climate and Nature Risk Management)

Why does this matter to banks?

At first glance, it may seem unusual that biodiversity has become a banking issue. But when examined more closely, the connection is actually very logical.

An agricultural company depends on soil quality, water availability, pollinators, and weather conditions. A food industry company depends on the stability of its supply chains. A real estate development or infrastructure project may affect protected areas, water reserves, or sensitive habitats. Mining, energy, or industrial investments may carry significant land-use, water-use, or pollution risks.

Sooner or later, these factors can turn into financial issues. They may affect permitting processes, operating costs, supply chain security, reputation, regulatory compliance, insurability, collateral value, and ultimately even a client’s creditworthiness.

In other words, nature loss is not merely a “green” or communications issue. If a company’s operations are highly dependent on natural systems — or if they significantly damage those systems — that may also represent a risk for the bank financing them.

What can banks expect from corporate clients?

Based on the European Central Bank’s good-practice guide, banks are approaching this topic in an increasingly structured way. This does not mean every client will be asked to provide the exact same dataset. Rather, banks are likely to examine higher-risk sectors, geographical areas, and activities more closely.

When assessing nature-related risks, banks may look at several aspects. For example, whether the client operates in protected or environmentally sensitive areas, has significant water usage, is linked to deforestation or land-use issues, depends on critical ecosystem services, or could have a material impact on endangered species and habitats. The assessment may also extend to the supply chain, especially in sectors such as food production, agriculture, forestry, textiles, construction, or mining.

More advanced banking practices are already moving beyond generic ESG questionnaires. Among the ECB’s examples are internal nature-risk scoring systems, sector policies, client rating criteria, project finance decision matrices, and client engagement processes. This means that nature-related risks may increasingly become embedded in actual financing decisions: loan approvals, loan conditions, ongoing monitoring, or even pricing.

The ECB also illustrates this through a client classification process flowchart: the collection of nature-related information is no longer treated as a separate “ESG side topic,” but rather as an integrated part of standard client due diligence, risk assessment, and lending decisions.

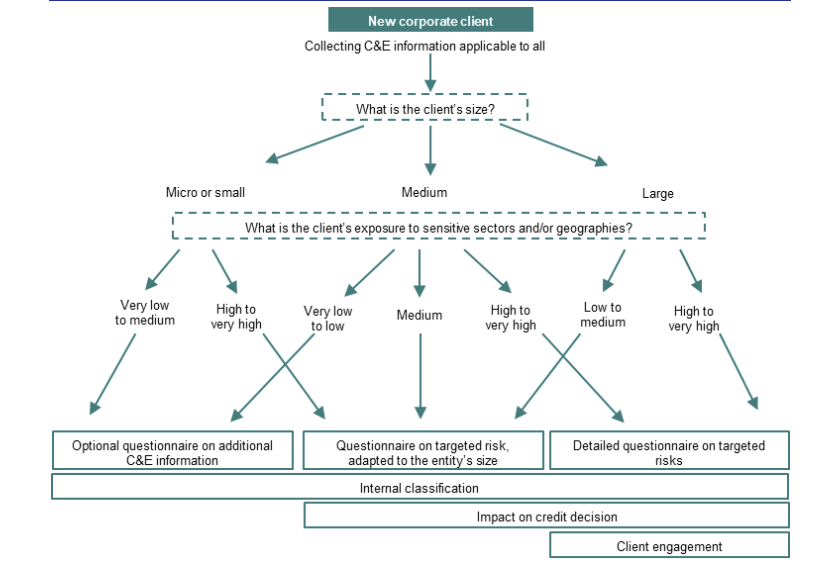

“Client classification process based on climate and nature-related risk considerations”

(Source: European Central Bank, Good Practices for Climate and Nature Risk Management)

This is an especially important message for companies. In the future, it may no longer be sufficient to simply state in general terms that “nature protection is important to us.” Increasingly, companies will need to demonstrate where a particular activity or project takes place, which natural systems it affects, what impact it has on biodiversity, and what measures are being implemented to manage those impacts.

The shift may be particularly visible in project finance

One of the most interesting application areas of nature-related risk assessment is project finance. In these cases, the bank evaluates not only the company’s overall financial position, but also the project itself: where it is located, what type of activity it involves, what environmental impacts it may have, and how manageable those impacts are.

Among the good practices presented by the European Central Bank is an approach in which banks assess the project’s environmental profile together with the client’s risk profile. A positive or low-risk project may proceed through a standard approval process, while a project with higher nature-related risks may require more detailed review, higher-level approval, additional conditions, or further engagement with the client. In the case of certain excluded activities, financing may not be available at all.

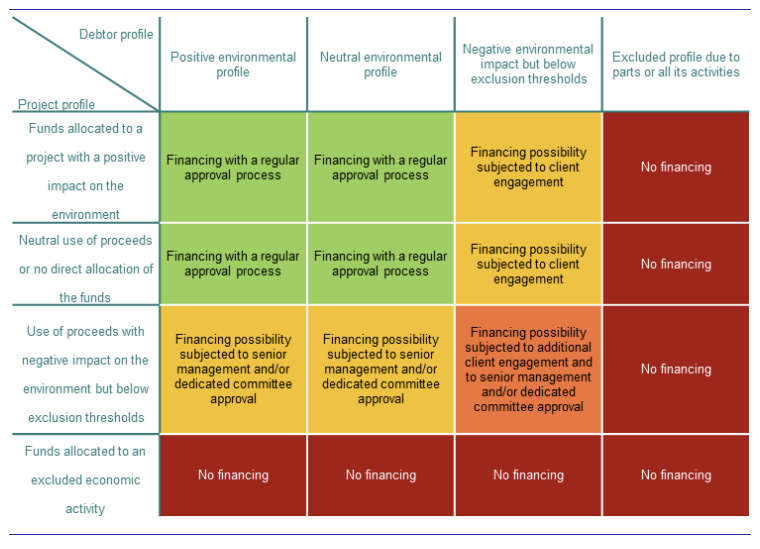

The ECB also illustrates this approach through a simple decision matrix. The key idea behind the model is that banks may evaluate not only the characteristics of the financed project itself, but also the environmental profile of the client or project sponsor. Together, these factors may determine whether financing can be approved through a normal process, requires additional conditions or client discussions, needs escalation to a higher decision-making level, or is ultimately considered non-financeable.

“Decision matrix based on the environmental profile of the project and the client”

(Source: European Central Bank, Good Practices for Climate and Nature Risk Management)

This perspective clearly shows that biodiversity impact assessment is no longer merely a reporting issue. Increasingly, it is becoming a source of decision-support information that may influence whether a project can be financed at all, under what conditions, and with what level of monitoring.

Nature is not only a risk — it is also becoming an investment theme

While nature loss is increasingly appearing as a risk on the banking side, another trend is emerging in investment markets: nature restoration, regenerative land use, and more sustainable forestry and agricultural practices are increasingly being treated as investment opportunities.

A good example is the Value Nature Fund I launched in April 2026 by Triodos Investment Management and Fondaction Asset Management. The closed-end natural capital fund targets a size of €300 million and focuses on regenerative agriculture and close-to-nature forestry investments across Europe, Canada, and the United States. The fund aims for an SFDR Article 9 classification and commits to measurable impact indicators in areas including biodiversity, ecosystem services, climate adaptation, and social well-being.

A similar direction is represented by HSBC Asset Management and Pollination through their joint platform, Climate Asset Management. This is not simply another “green fund,” but a natural-capital-focused asset management platform investing in sustainable forestry, regenerative agriculture, and nature-based carbon projects. The example demonstrates that nature-related investments are not interesting solely from an environmental perspective: the goal is to make nature restoration, land-use transformation, and ecosystem resilience financially viable investment strategies.

The Mirova Sustainable Land Fund 2 also fits into this trend. With a target size of €350 million, the fund invests in sustainable forestry, agroforestry, and regenerative agriculture projects with the aim of generating not only financial returns, but also positive impacts on climate, biodiversity, water resources, and social inclusion.

These examples do not mean that nature has suddenly become just another “investment product.” Rather, they show that financial markets are beginning to recognize that the condition of nature carries economic value. Soil fertility, water availability, forest resilience, pollination, habitat quality, and ecosystem stability are all factors that ultimately influence long-term economic performance.

Why measurement will become critical

Whether we are talking about bank lending decisions, project finance, or investments in natural capital, the key question remains the same: how can nature-related impacts and risks actually be measured?

This is not an easy task. Compared to carbon emissions, biodiversity is far more complex. It cannot be captured in a single tonnage figure or one universal metric. The location matters, the ecosystem type matters, the nature of the activity matters, as do water use, land use, pollution, habitat conditions, species impacts, and the preventive or restorative measures applied by a project.

This is exactly why structured, activity- and project-based assessment will become increasingly important. Companies and banks will need information that goes beyond generic ESG statements and helps them understand what nature-related risks a specific activity carries, how it affects biodiversity, and where the most important intervention points lie.

On the corporate side, this process is reinforced by frameworks such as European Sustainability Reporting Standards ESRS E4, which focuses on biodiversity- and ecosystem-related impacts, risks, and opportunities, as well as the Science Based Targets Network (SBTN), which encourages companies to adopt science-based targets for nature. These frameworks do not need to be explored in detail here, but they clearly show that the corporate and financial worlds are moving in the same direction: nature-related impacts increasingly need to be understood, measured, and managed.

The ability to measure nature-related risks may become a competitive advantage

On Biodiversity Day, it would be easy to speak only about the moral responsibility of protecting nature. And that responsibility is real. But today, the issue goes far beyond ethics.

The condition of nature is becoming an economic factor. Nature loss can create operational, supply chain, legal, reputational, and financial risks. At the same time, nature restoration is increasingly becoming a matter of investment, resilience, and competitiveness.

For banks, this means that nature-related risks can no longer remain buried in the appendix of sustainability reports. They need to be integrated into client assessment, lending processes, portfolio analysis, and strategic decision-making.

For companies, this means it is worth preparing early. In the future, the businesses and projects with the strongest position may be those that not only speak generally about nature protection, but can clearly demonstrate what impact they have on their environment, which risks they manage, and what concrete measures they take to preserve or improve the condition of nature.

The question is therefore no longer whether biodiversity matters. The real question is whether we are capable of recognizing, measuring, and integrating nature-related risks and opportunities into decision-making in time.

Because what still appears to many people today as merely a sustainability topic may tomorrow become a financing condition, an investment criterion, or a source of business competitive advantage.