Alongside the rapid growth of the green bond market, credibility is becoming increasingly important. The EU Green Bond Standard (EUGB) establishes a unified framework for taxonomy alignment, mandatory external verification, and transparent reporting. The quality of sustainability performance and ESG data is increasingly influencing financing terms and access to capital.

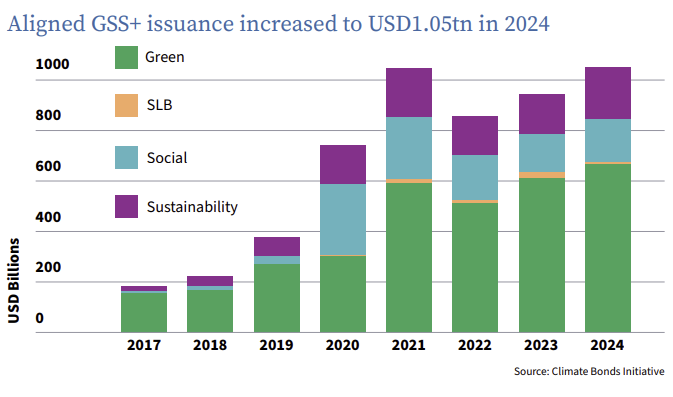

The sustainable finance market has expanded rapidly in recent years, with green bonds becoming one of the most important financing instruments for climate and environmental investments. According to data from the Climate Bonds Initiative, in 2024 approximately USD 670 billion worth of green bonds were issued globally, while the total sustainable bond market approached USD 1.1 trillion. In Europe, green bonds accounted for 6.9% of all bond issuance, highlighting that sustainable finance has become a significant segment of the capital markets.

Global Volume of Green Bond Issuances

With the rapid growth of the green bond market, a fundamental question has become increasingly prominent: what makes a green bond truly “green,” and how reliable are the sustainability claims disclosed by issuers?

In response to this challenge, the European Union created the EU Green Bond Standard, introduced through Regulation (EU) 2023/2631. The regulation was adopted on November 22, 2023, and came into effect on December 21, 2024, establishing a unified, regulated framework for “European green bonds” (EUGB).

This change goes beyond capital markets. It is increasingly clear that sustainability performance and the quality of ESG data directly affect companies’ access to financing — whether through bonds, bank loans, or investor perception.

EU Green Bond Standard: a new level of credibility

The EU Green Bond Standard aims to provide a uniform, transparent, and comparable framework for green bonds. The system is voluntary; however, the term “European Green Bond” (EUGB) may only be used if the issuer meets the requirements of the regulation.

The standard is built around four key elements:

- Alignment with the Taxonomy: at least 85% of proceeds must finance projects fully compliant with the EU Taxonomy criteria.

-

Detailed disclosures and reporting on the use of proceeds and environmental impacts.

-

Mandatory external verification by certifiers registered with the European Securities and Markets Authority (ESMA).

-

Standardized templates to improve comparability for investors.

While the framework is strict, it allows practical flexibility: up to 15% can be allocated to a so-called “flexibility pocket” for activities where taxonomy criteria are not yet fully met, provided the do no significant harm (DNSH) principle and minimum social safeguards are still applied.

The message is clear: sustainability in financial markets is increasingly an auditable performance, not just a communications claim.

Rapid market response

The practical significance of the regulation is evident from the quick adoption by major financial institutions. Deutsche Bank recently announced its first green bond structured according to the EU Green Bond Standard (EUGB), with proceeds allocated to taxonomy-aligned financing activities.

Early issuances show a strong positive market response. In the first months, more than twenty issuers entered the market, totaling around €20 billion. The Italian company A2A’s bond was oversubscribed more than four times, while the European Investment Bank’s €3 billion issuance attracted nearly €40 billion in investor demand.

Initial concerns that strict requirements might constrain the market have not materialized.

Evolution, not revolution

The green bond market has already been operating, primarily guided by the ICMA Green Bond Principles. Compared to that, the EUGB does not introduce a completely new logic, but rather:

-

Creates a closer link to the EU Taxonomy,

-

Applies a uniform disclosure structure,

-

Strengthens the role of external verification,

-

Increases data comparability for investors.

It is also important that market infrastructure — settlement, distribution, and custody systems — is already prepared for these new issuances. The change primarily affects transparency and data quality rather than the basic market mechanics.

Operational side of green finance: the role of the framework

In practice, issuing a green bond is not a single transaction but the result of a complex preparation process. Central to this is the corporate Green Finance Framework, which documents:

-

Eligible project categories,

-

Project selection processes,

-

Segregation of proceeds,

-

Allocation and impact reporting systems,

-

Methods of external verification.

For investors, this framework provides the basis for transparency and accountability; for issuers, it ensures the integration of sustainability strategy into financial practice.

The bigger trend: financial relevance of ESG data

The EUGB is part of a broader financial shift. Banks and regulators increasingly recognize that physical and transition risks related to climate change manifest directly as financial risks in institutional portfolios — as credit risk (e.g., business model vulnerabilities), market risk, or operational risk.

Consequently, more financial institutions are integrating ESG factors into credit rating and risk management processes, and sustainability performance increasingly influences financing conditions. For instance, Norway’s DNB plans to use the VSME framework to support SME credit assessments, providing proportional, actionable ESG data for decision-making. (Although Norway is not an EU member, its connection to European financial markets makes EU sustainable finance standards a practical market reference.)

The European Central Bank also emphasizes that high-quality sustainability data is essential for financial stability and efficient capital allocation.

Financing costs are changing

Market experience shows that credible green finance can come with more favorable terms (“greenium”). This phenomenon increasingly applies to issuances that are:

-

Taxonomy-aligned,

-

Accompanied by detailed impact reporting,

-

Externally verified,

-

Supported by a strong corporate sustainability strategy.

In other words, better financing terms depend on high-quality ESG data and strong governance.

What this means for companies

The conditions for green financing are tightening, and companies that succeed will be those capable of:

-

Applying the EU Taxonomy,

-

Collecting reliable environmental data,

-

Measuring the impact of investments,

-

Operating a structured ESG governance system.

In practice, sustainability is no longer a separate communications topic; it is becoming a financial and risk management competency.

For small and medium-sized enterprises, it is particularly important to recognize that the demand for ESG data extends beyond capital markets. In bank lending, sustainability performance increasingly affects financing conditions as well.

Where is the Green Bond Market Heading?

Based on current developments, several trends are emerging:

-

The EUGB may gradually become the default standard for high-quality issuances.

-

Investors are increasingly seeking taxonomy alignment and verified data.

-

Financing terms are becoming more differentiated based on sustainability performance.

-

The quality of sustainability reporting can directly impact access to capital.

-

Integration of ESG information into credit, bond, and investment decisions will continue to strengthen.

Conclusion: Sustainability as a Financial Infrastructure

The introduction of the EU Green Bond Standard clearly signals that sustainability has become a structural element of the financial system. For companies, the question is no longer whether to collect and report ESG data, but how to do so — with what quality and strategic approach.

Experience shows that sustainability performance and data quality increasingly determine:

-

Financing costs,

-

Investor confidence,

-

And, in the longer term, the company’s competitiveness.

The “gold standard” for green bonds is therefore more than a new market instrument. Sustainability information is gradually becoming a core part of corporate financing infrastructure, and organizations that prepare early for this new operating environment will gain a competitive advantage.

Free Expert Consultation

Sustainable finance and ESG expectations are evolving rapidly. Increasingly, companies are facing requests from banks, investors, or business partners for sustainability data — whether in the context of green financing, credit assessments, or supplier compliance.

If you are uncertain about:

-

Whether you need to collect ESG data or prepare a report,

-

How CSRD, the EU Taxonomy, or other sustainability requirements affect your company,

-

How sustainability relates to financing opportunities,

-

Which steps are actually necessary (and which are not),

it is worth clarifying your situation in a short professional consultation.